Can CATL continue its global rise?

Can CATL continue its global rise?

How politics is shaping its future of the Chinese battery giant

With a market capitalization larger than General Motors and Ford combined, Contemporary Amperex Technology Limited, aka CATL dominates the global lithium-ion battery sector. Not bad for a company only created in 2011. The explosion of the electric car market and the promise of further growth as has allowed CATL to become a global behemoth supplying car manufacturers with cheap batteries.

CATL is particularly dominant in the Chinese market but has successfully exported to car makers across the globe. CATL now controls a global spider’s web of supply chains and manufacturing bases making it a geopolitical player in its own right, albeit under the watchful eye of Beijing.

China’s Dominance

The Chinese government has succeeded in its quest to dominate the global battery industry. Now its aim is to maintain and extend that lead as electric cars steadily overtake traditional models. CATL’s successful strategy has been to sacrifice performance (range) for a lower price by using previously unfashionable lithium-ion batteries. With 18,000 research staff and an R&D budget of around US$2 billon CATL is planning to stay ahead of its rivals in terms of technology and price.

CATL has also bucked the recent trend of declining Chinese investment in the US. By signing a US$3.5 billion deal to build a battery plant in Michigan with Ford – it has also sent a signal of continued confidence in what has been a rocky international relationship. The deal has drawn scrutiny from many in the US who fear Chinese involvement in the heart of what is an emotive industry for many Americans. Although CATL is a listed firm, all companies in China ultimately answer to Beijing.

Competition

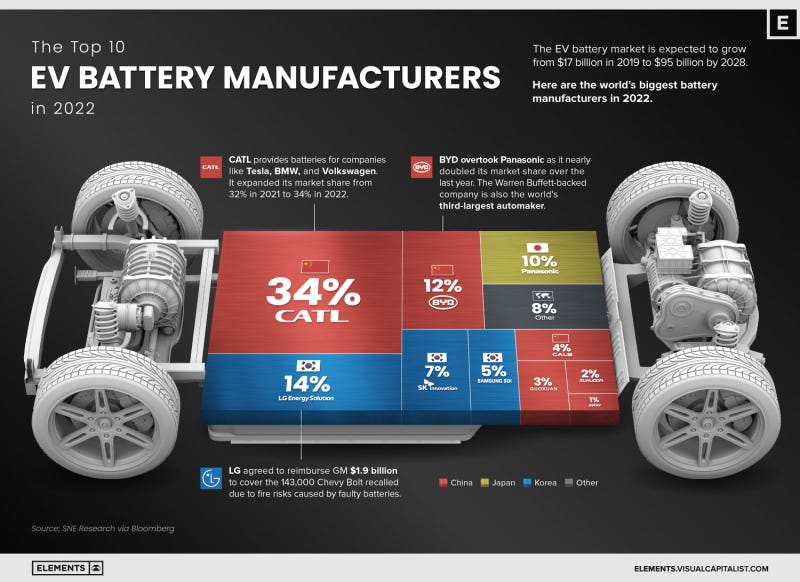

Foreign policymakers are concerned about CATL’s global dominance. The firm’s 37 percent global market share gives it considerable leverage when buying raw materials. CATL’s dominance also means China’s dominance. This is particularly apparent when you consider that other Chinese manufacturers overall dominate the sector.

CATL together with BYD (third biggest manufacturer) make up nearly 50 percent of the global market. Both companies can produce batteries extremely cheaply, less than $60 mm per megawatt hour, giving for now at least a significant edge over rivals. Other producers like Panasonic or LG have to rely on superior performance to gain customers.

Many are worried that Chinese firms will snuff out the competition at a critical juncture when the battery sector is blooming. This will leave the rest of world dependent on Chinese batteries.

Alternative Batteries

The EV battery industry is still relatively young. New types of battery like sodium-ion are emerging. While new markets such as for large scale grid storage are also now growing fast. This and many other factors could change the dynamic of the battery market. As more electric cars are built the market will grow fast and in perhaps unpredictable ways. Electric cars represented 14 percent of global new car sales in 2022, up from 9 percent in 2021. This represents a fast-growing market, but one which has a long way to grow.

Rival companies such as Japan’s Panasonic and South Korean’s LG Energy and are increasingly betting their future on nickel heavy batteries. These batteries include a cathode containing nickel, manganese and cobalt. Nickel rich would be a more accurate description. The firms backing (such as Panasonic) them are backing them thanks to superior performance, in particular a longer range (which is important for US drivers who often cover long distances).

Nickel batteries are currently more expensive, so much depends on new nickel supplies (especially in Indonesia) coming online and bringing the price of the metal down. There is also excitement about the emergence of solid-state batteries which promise improved performance and could be used for lorries or even planes. Toyota has claimed a breakthrough in solid-state technology and promises large scale production in 2028.

Geopolitical Hinge

Developments in technology are important but the future of batteries also hinges on geopolitics. The US and EU realise their dependence on Chinese manufacturers and want to develop their own reliable battery supplies from friendly countries or domestically. Currently all top ten battery manufacturers are Asian companies. At the same time, they are currently dependent on these same manufacturers to meet decarbonisation goals.

The next decade will witness the rise of the electric car and there will be a battle between corporations and countries to control what will be a cornerstone of the global economy. As Europe and the US shift towards electric cars this could be the opportunity for Panasonic and LG to gain market share from CATL, as companies from friendly countries like South Korea and Japan will be increasingly favoured over Chinese rivals particularly if US-China relations remain frosty.

GM’s major rival Ford has recently completed a deal to secure a large proportion of raw materials from North American suppliers. At the same time Ford risk losing a tax credit only available to domestically produced cars. This underlines the importance of the US IRA legislation that will shape business decisions and shift production of batteries and other climate tech away from China by giving domestic producers generous subsidies and tax breaks..

Conclusions

The future of batteries will be driven by the decisions and actions of mining companies like Glencore, Vale and Rio Tinto, car manufacturers like Tesla, Nissan and Volkswagen that produce cars and batteries, or others like Yutong or Zhongtong that just produce cars but not batteries.

These firms are playing an intricate game against a backdrop of shifting policy changes determined by governments and the commercial dynamics of the battery market. Whoever can build the most favourable alliances, develop the most cutting-edge technology and take advantage of the policy environment will emerge the winners.