China’s Drive for Energy Security

How China’s desire for security drives its energy strategy

While visiting the Shengli Oil Field in the Yellow River Delta in 2021 Chinese President Xi remarked that:

“China must hold the energy food bowl in its own hands”.

These words made to oil workers neatly sum up China’s energy policy objectives. The visit coincided with the launch of China’s 1 + N strategy which outline efforts to achieve net-zero by 2060. But behind the drive for carbon neutrality and much criticised building of new coal plants lies a deeper strategic goal. China desperately wants to avoid overdependence on other country’s energy resources. To find why I take a look at the past, present and future of China’s energy policy.

Powering China’s Rise

The spectacular rise of the Chinese economy was forged in the factories, industrial sites, and gargantuan infrastructure developments built across China in the last 40 years. It was also built on the back of inexpensive energy. Cheap energy has been the key to industrialisation (and wealth) ever since easy access to coal kickstarted the original industrial revolution in Britain 200 years ago.

Supplies of cheap coal have also been key to China’s industrial rise, but a modern economy also requires huge volumes of oil and gas. China soon outgrew its domestic oil supplies and became a net oil importer in the 1990s. After decades of isolation Chinese firms soon viewed the world as a giant marketplace and by the 1990s were investing in, mining for, drilling, and buying raw materials across the globe. This graph shows oil imports increasing year on year, except the recent Covid induced economic downturn.

Belt and Road

This strategy soon morphed into the Belt and Road Initiative (BRI). Importing so much oil and gas placed the Chinese government in a strategic dilemma – its economy was now highly vulnerable to disruptions or blockades. In particular, any dispute over Taiwan, or with Japan, could result in the intervention of the US Navy which would cripple its economy. Energy security soon became a major political issue within the Government. How could China power its economy but maintain its resiliency and security?

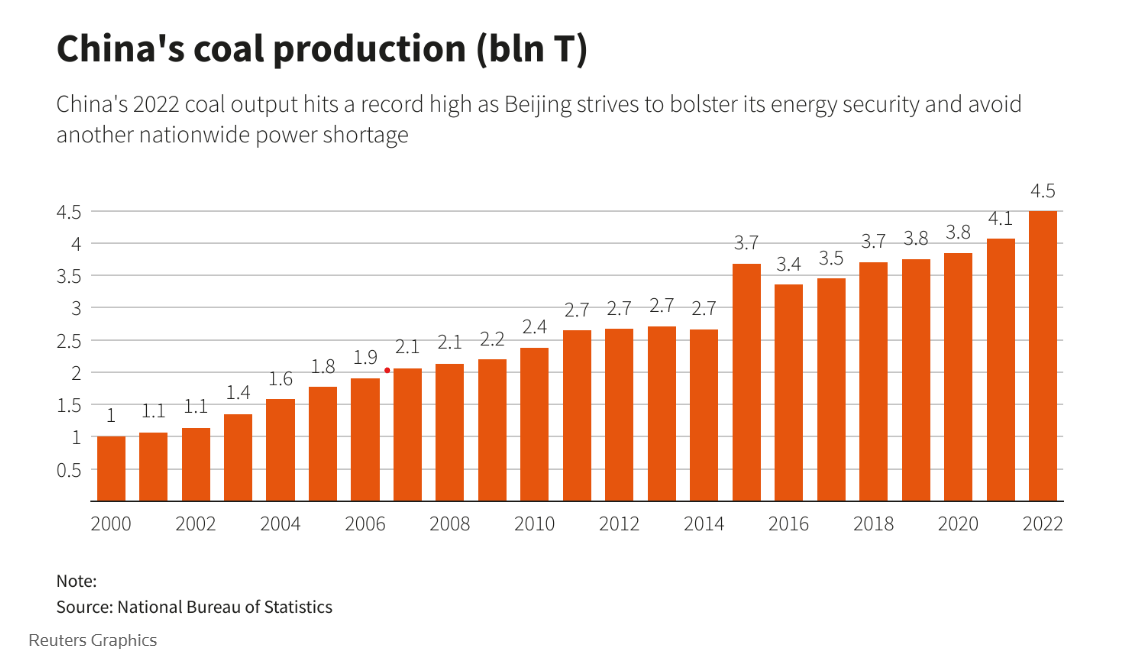

King Coal

China’s approach to this dilemma has been multi-pronged. Firstly, China has huge reserves of coal which despite the devastating carbon emissions and deadly pollution has been the backbone of the nation’s electricity supply for many years. Burning coal is an ingrained habit but is now at an inflection point.

Growing solar power is undercutting the price of coal and the pressure to decarbonise is undermining its long term position. China continues to build new coal plants but strangely it is likely that these will be used less intensively and increasingly as back-ups for renewable sources. Coal plants are also a key plank of energy security. Should other forms of energy fail, China can fall back to its coal reserves.

China has also heavily tapped into hydropower most notably with the Three Gorges Dam. The country is also planning further nuclear power plants – more than any other nation. But these are relatively expensive options in terms of capital. However, they are extremely welcome from a energy security point of view as they are largely dependent of other countries.

Peak Oil

Coal cannot provide all China’s energy needs. Oil and gas are needed to run cars, heat homes and provide a wide range of different products based on oil. This quest for oil led China to the Middle East from where it imports like much of the world vast quantities of hydrocarbons.

China has also cultivated close relations with many African oil producers. Chinese firms like Sinopec backed projects that many western companies avoided thanks to regional conflict and messy local politics. Chinese oil giants invested in projects across Angola, Sudan, Gabon and many other nations despite the political risk.

The Price of Oil

At current prices oil is expensive and for China its supply route is the most vulnerable to attack. To reduce dependence on the Middle East, China is looking to buy more oil and gas from Russia and Central Asia. Pipelines across Eurasia are much less vulnerable than sea routes. Russian gas supplies to China are expected to increase with the completion of a new gas pipeline Siberia 2 – which will cross through Mongolia.

This pipeline will join the Power of Siberia route which has been operating since 2019. Russia of course is desperate to shift its oil and gas exports East and avoid dependence on Europe. This is ideal for the Chinese government who knows they can extract a good price from Moscow. Indeed analysis suggests that Russia is already paid less than Turkmenistan for its gas supplies.

The Great Transformation

The Chinese government’s decision to prioritise the development of renewable technology base now looks to be a momentous one. By backing renewable energy technology, most notably the manufacture of solar panels, wind turbines and electric car batteries, China now rules these markets. As a result, China also dominates the supply chain of strategic minerals and metals via a global network of mines, processing plants, ports and factories supplying the new components of the net-zero economy.

Renewables Rise in China

China has seen the rapid uptick in electric vehicles and buses helping to reduce pollution in its cities. The spectacular rise of solar energy – (capacity doubling last year) is transforming China’s energy mix. From an energy security point of view solar energy and electric cars are ideal. The only vulnerability is that China is dependent on foreign imports on strategic or critical materials like cobalt, copper and nickel.

Critical Supply Chains

However, in comparison to oil flows which can be disrupted almost instantly if say Saudi Arabia cuts production, or because of a war in the Gulf or a naval blockade. If supplies of strategic materials are cut-off then it will stop or increase the cost of new solar panels. But it does not affect existing solar panels which will carry on generating power regardless. Oil producers have far superior geopolitical leverage compared to critical material suppliers.

There are strategic considerations with some metals: nickel production is concentrated in Indonesia; Lithium in South America and Australia. Any geopolitical risks can cause price spikes. But given China’s dominance and deep involvement in these markets it has an effective hedge on political risk. In comparison, US, European and other climate tech manufactures are very much in Chinese hands.

For now China’s quest for energy security is still out of reach. Its addiction to oil and coal means will take a long time to wean itself off fossil fuels. One sting in the tail is that if it does ever achieve or get close to energy independence, it could make China less vulnerable and more tempted to make gambles like an invasion of Taiwan.