Critical Materials, Energy Transition and Geopolitics

A Guide

In 2010, a Chinese fishing boat collided with a Japanese coast guard vessel close to the disputed Senkaku Islands in the Pacific. After the crash the fishing boat captain was detained by the Japanese authorities. The Chinese government soon called for his release, and when Japan failed to comply, Chinese exports of rare earth metals were halted. China did not officially ban their exports, instead they were delayed at ports requiring further inspections.

Rare earth metals are a group of metals which are not actually that rare; but are vital for the production for much modern technology such as electric batteries.

Japan perhaps concerned that the lack of rare earth metals would disrupt the production of iconic cars like the Toyota Prius soon released the captain and exports resumed. However, the episode brutally highlighted Tokyo’s dependence on rare earth metals imports from China. The Japanese government rapidly spearheaded efforts to diversify the supply of rare earth metals from the likes of Australia, but dependence on China remains.

Why are Critical Materials so critical?

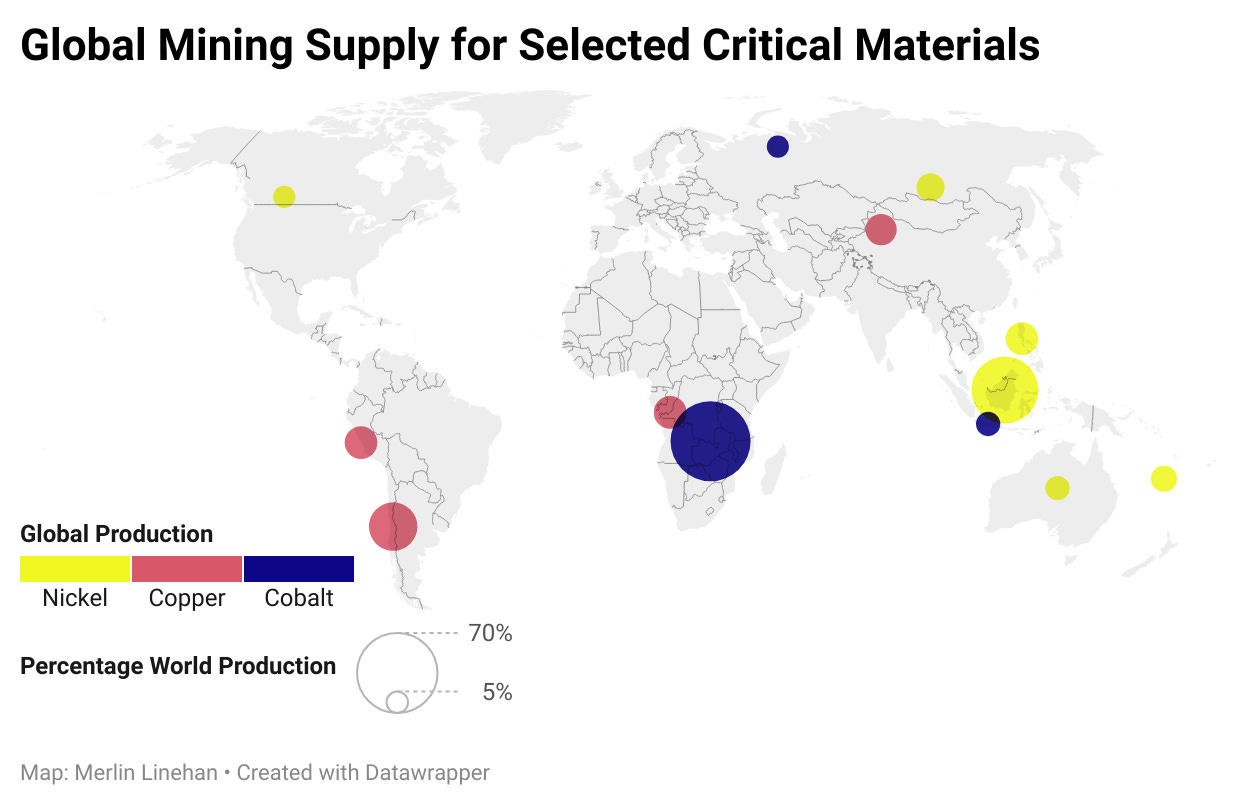

There is no exact definition for Critical Materials. Any list typically includes copper, lithium, cobalt, rare earth metals and graphite. But why are critical materials important? Put simply critical materials are the stuff needed to build modern climate technology, such as batteries, solar panels and wind turbines. Critical materials are also a key part of many common items, mobile phones, laptops as well as many defence, electronic and other uses.

China realised the importance of these materials knowing that building a climate technology industrial base would give them a competitive edge as the world shifts away from fossil fuels towards renewable energy.

To build this industry, the country would require a cheap reliable source of raw materials. This is part of the reason Chinese firms have been so active in the mining, refining and import of critical materials across the world.

New Competition

Now other countries are waking up to China’s lead in climate technology and dominance of the critical material supply chains that feed it. Over time as the spread of climate technology gains momentum the importance of critical material supply chains will become of growing geopolitical importance. Geopolitical competition and collaboration driven by commercial demand will help shape the future of critical material supply chains.

As different countries realise the importance of critical materials a range of different policies, legislation and government action is emerging in an attempt to try and diversify critical material supply chains.

National Policies

Across the globe different countries are implementing policies and laws to ensure a reliable supply of critical raw materials:

The EU’s Critical Raw Material Act is a major step forward in ensuring the EU has access to critical materials to feed its climate technology sector which has fallen behind China. The Act set out clear priorities to diversify sources of critical materials and develop strategic relationships with reliable partners.

The Act sets targets for 2030: Crucially, that not more than 65 percent of each raw material will originate from a single non-EU country and that certain large companies will have to audit their critical material supplies to ensure resilience. The EU also plans to engage with critical mineral suppliers via its Global Gateway Strategy.

Another proposed action is a Critical Raw Materials Club which could bring together like-minded countries (read Western aligned) to discuss and resolve issues in the supply chain. The Act also sets targets designed to encourage the recycling of critical materials, which is a painstaking and difficult process, but will become more prominent as the EU also encourages a circular economy.

Inflation Reduction Act in the US is a huge piece of legislation covering many areas, tax, expanding energy use, but there is also a section covering critical materials. Firms that can source critical materials from “friendly” countries – will benefit from generous tax credits. Friendly is defined as having a free trade agreement (FTA) with the US – which has caused some tensions with countries lacking an FTA.

The US government strategy is that supply chains will shift towards the US in tandem with a fast growing climate tech sector. The US is also pursuing agreements: bi-lateral agreements with Japan, the EU and the UK look to facilitate trade between these countries, increase environmental protections and prevent restrictions in the export/import of critical materials between them.

Mining countries led by Indonesia are banning unprocessed ore in many cases, as they want ensure the refining of metals and mineral is done in country helping to dsevelop a manufacturing base. Some want to go further and develop climate tech manufacturing capacity. There is a global trend towards protectionism in critical materials. Zambia and Namibia have also banned raw lithium. While Mexico and Chile are looking to nationalise or at least increase the state’s role in the lithium industry.

Canada’s Critical Mineral Strategy: Canada is in the envious position of hosting enormous mineral wealth. Canada’s graphite, lithium, cobalt, and nickel has attracted a great deal of interest from climate tech manufacturers. It is no surprise that Canada has a strong pipeline of new mineral projects and looks set to benefit as a reliable supplier especially to the US market. However, new mines often attract opposition on environmental grounds.

Canada also wants to present itself as a sustainability leader in extractive industries. One important question is whether the benefits from mining will outweigh the costs to indigenous people and biodiversity. Canada is in competition with miners in Africa, Latin America and China which have weaker environmental and social protections.

Australia is in a similar position to Canada. As a major mining power, the country is an excellent position to provide the likes of lithium, rare earth metals and other materials to friends and rivals alike. However, Australia can like Canada market itself as a reliable supplier to western countries that will be un-swayed by pressure from Beijing. Canberra is also looking for new sectors that will provide economic opportunities given the expected decline in coal mining. An inevitable result of a world moving away from fossil fuels.

In the next post I will look at how the dynamics of the critical material supply chain present a threat to many companies, and how they can identify and act on this to reduce their risk.