How Climate Finance Works

Financing the Green Energy Revolution

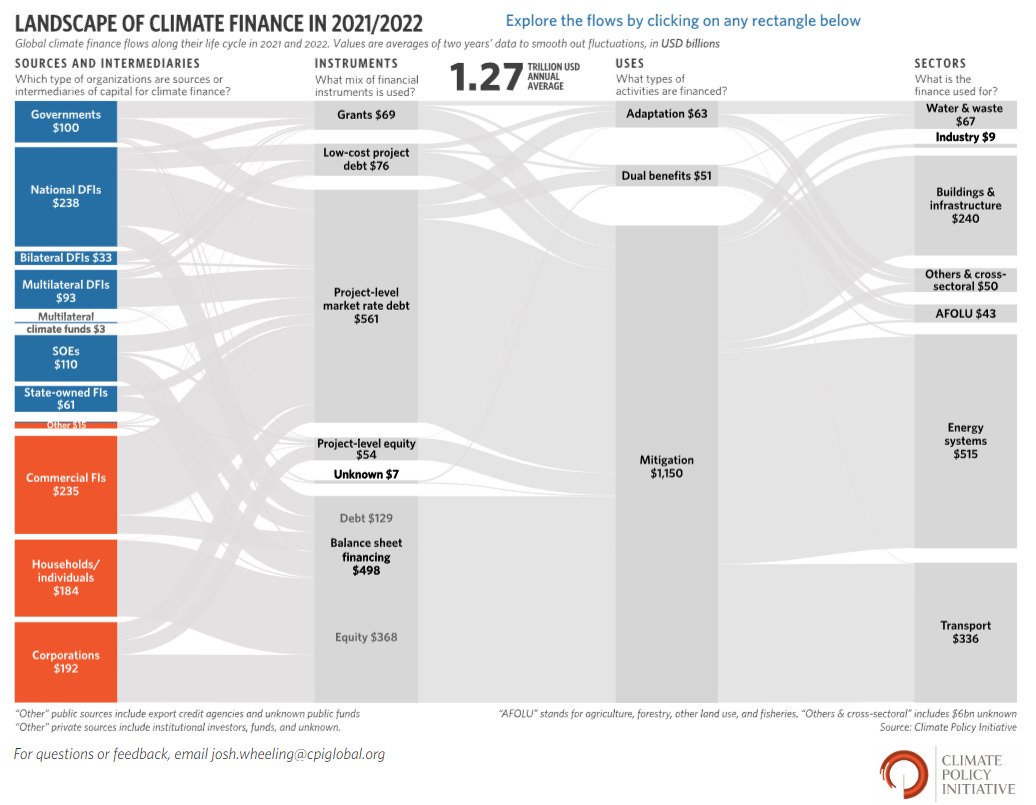

Global climate finance flows doubled in two years to reach US$1.3 trillion in 2022. A major success no doubt. But the estimated amount per year to achieve global climate goals and transition to a net-zero economy are in the region of an eyewatering US$ 9 trillion a year.

The global energy transition is powered by climate technology such as solar panels, batteries and wind turbines. But all of this is wheeled with money. Put simply, if projects, technology and innovation are not backed by banks, or governments or some kind of finance they simply won’t happen.

Funding for renewable energy has multiplied in recent years as banks view a unique opportunity to fund the shift to net-zero. But the astronomical sums needed to shift away from fossil fuels and decarbonise the economy means there is a massive funding gap. How can this gap be closed and where does politics come into it?

Where is the money going?

The Climate Policy Initiative provides an amazingly helpful and attractive overview of climate finance.

Approximately half of climate finance comes from the private sector. Banks and other financial institutions lead the way, closely followed by corporations. Amazon is the by some measures the biggest backer of renewable energy in the world with over 500 wind and solar projects across the world.

The private sector is in providing climate finance. Overall, the best way to encourage this is more commercially viable climate finance projects. How does this happen? Firstly, the falling cost and increasing efficiency of renewable energy is making the sector increasingly attractive.

But Governments can also play their part. Policy changes such as the Inflation Reduction Act and the Production Linked Incentives in India promote climate tech through subsidies, tax breaks and incentives. As a result, US and Indian renewable energy manufacturing (especially solar) are booming. Build an attractive policy environment and the money will follow.

DFIs

Public finance provides the other half of climate finance. Leading the way are National Development Finance Institutions (DFIs). These often-unsung heroes of finance are state owned finance organisations which typically back projects that are unfeasible for the private sector. KFW in Germany is a classic example of a DFI and around a third of its funds go towards climate-based goals.

There are many more DFIs around the globe and they can continue backing the growing demand climate finance, but will need government backing to increase their commitments. Government themselves are major backers of climate finance (US$ 100 billion a year), so DFIs are both competing with, and complementing government spending.

State Owned Enterprises

State Owned Enterprises (SOEs) are the next biggest source of finance. Any discussion of SOEs usually begins with China. The Chinese corporate scene is dominated by these giants of industry which are wholly or partly owned by the government.

Although often derided as dinosaurs with inefficient and outdated practices they remain the ideal vehicle to support government policy. The Chinese government’s Five-Year plan has committed these SOEs to a 50 percent increase in renewable energy generation by 2025. This top-down approach has been criticised for its bluntness and for some SOEs unaccustomed to green energy, it will be a culture shock, but it gets results.

SOEs like Sinopec, Guodian Energy and Longyuan Energy are pivoting towards or are focused on renewable energy. China’s ability to force SOEs to commit to clean energy has seen the country double its solar energy capacity in one year.

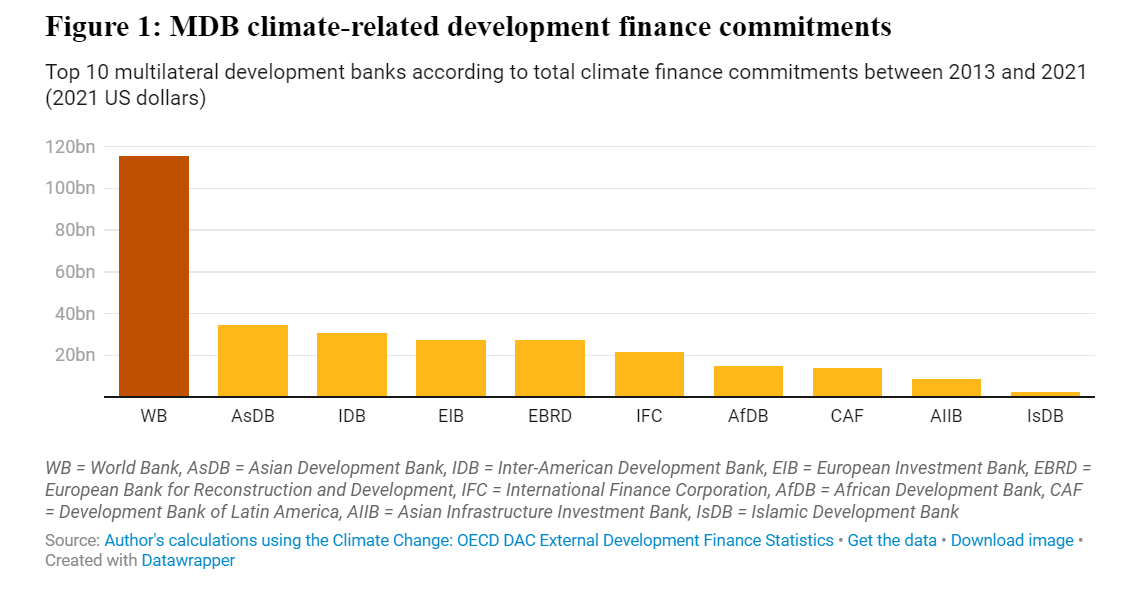

Multilaterals

Next on the list are multilateral finance institutions like the World Bank and Asian Development Bank. These organisations are typically focused on emerging economies, which gives them a unique role. Because most climate finance is focused on wealthier countries, the role of multilateral IFIs to both fund climate finance and encourage positive policy change in the developing world is crucial.

Mitigation Rules for now

Mitigation gobbles up nearly all climate finance (US$1,150 trillion in 2022) funding. In other words money is spent on reducing carbon emissions through clean energy or low/zero carbon technology.

We can expect to see this figure go up over the next decade as renewable energy and low carbon technologies spread. But we will also see mitigation funding increase rapidly from a currently miniscule US$ 63 billion as the impacts of climate chaos hit and communities are forced to adapt and upgrade infrastructure built for a different world.

Sectors

It is no shock that most climate finance goes towards the energy (US$515 billion) and transport (US$ 336 billion) sectors. Shifting away from fossil fuels in producing energy is the lowest hanging fruit and we can expect these sectors to continue receiving the most funding. Overtime as technologies improve and innovations arrive we can expect to other areas start getting a bigger slice of the pie.

What else can be done to close the finance gap?

Perhaps surprisingly one of the most effective measures to promote climate finance is for governments to actually spend less. Global fossil fuel subsidies stand at an incredible US$ 7 trillion. These are a mixture of explicit subsidies where governments spend to decrease the price of oil, gas or coal to help consumers (or voters!) and businesses. Implicit subsidies are social and environmental costs imposed by fossil fuels in terms of pollution (healthcare costs), and of course climate change.

Dropping fuel subsides can be politically unpopular in many countries, but it not only saves the government money, it also helps the shift to renewables alternatives. Nigeria dropped fuel subsidies in mid-2023, an unpopular move which tripled fuel prices overnight. The cost of running small generators used by many to cover blackouts became untenable. As a result many are switching to solar panels – a natural choice in a sun blessed country.

Cutting fossil fuel subsides saves government’s money which can then be used to back renewable energy. Soon I will cover alternative sources of finance such as climate venture capital and sovereign wealth funds in more depth, plus a look at how and why China finances energy projects along its Belt and Road Initiative.