Why the battle for critical materials is heating up

The global energy transition is creating new geopolitical tensions

200 kilos of copper, lithium, nickel, manganese, cobalt, graphite, zinc and rare earth elements are needed to build a modern electric car. Demand for these materials is rapidly increasing and not just for electric car batteries, but for many other technologies that are a regular part of daily modern life such as laptops and phones.

Now China is threatening the US, Japan and the EU’s electric car industries by imposing restrictions on the export of raw materials and technology. To understand why China is doing this first we need to look at the trade in semi-conductors and Sino-US relations.

Chip Wars

Growing geopolitical tension between China and the US evolved into a trade war during the Trump administration and relations remain frosty in the Biden era. Many believe the relationship has transformed into a 21st century version of the Cold War. China is trying to dismantle the US led global order, while the US increasingly tries to thwart China’s rise.

Both sides use tariffs, investment restrictions, espionage, and many other tools short of open warfare to gain an advantage in their struggle for diplomatic, economic and military supremacy. The US administration has correctly viewed the semiconductor industry as one where they can exert maximum leverage against China.

Semiconductors – the lifeblood of the modern economy

By preventing China from accessing the latest in semi-conductor technology the US gains a major competitive advantage in hi-tech industries, modern weaponry and in particular using artificial intelligence (AI). The cutting edge of AI relies on advanced chips with powerful processing power to complete tasks. At US bidding its allies in the Netherlands and Taiwan stopped China from importing these prized chips.

After it was cut out of the advanced chip trade China will continue to develop its own domestic semi-conductor industry. But the cutting edge technology built by the likes of NVIDA and ASML take years of development and research before they are manufactured. This process is not easily replicated.

The US has successfully (for now) controlled the supply of hi-tech chips, but this move places a further chill on Sino-US relations.

The PRC Strikes Back

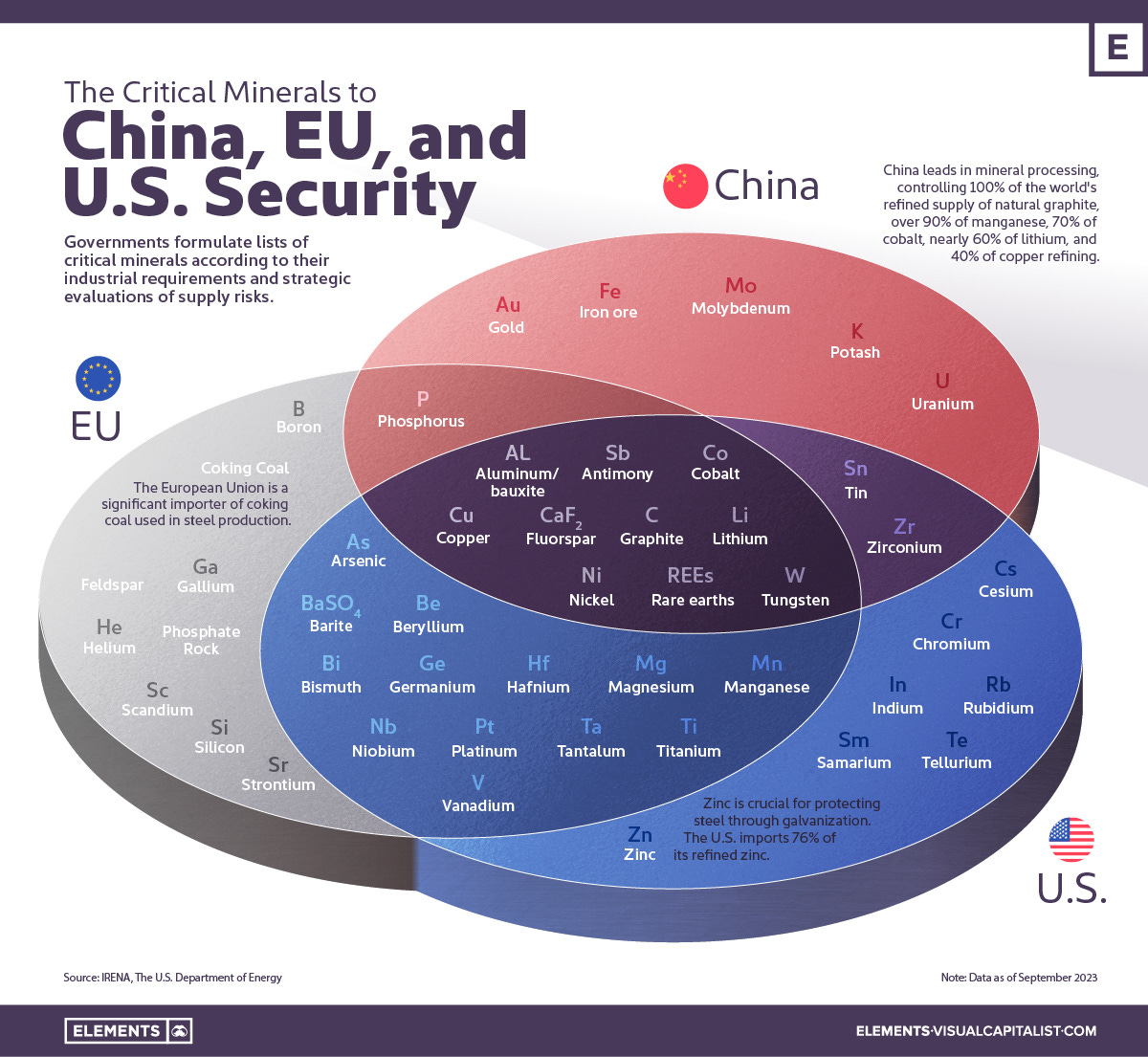

Beijing is not helpless in this trade war and has many ways to strike back at the US. China’s dominance of the climate tech sector means it dominates much of the supply of raw critical materials. Chinese firms control lithium processing in South America, cobalt mining plants in Central Africa, and much of the world’s supply of rare earth metals.

This gives China the luxury of cutting the supply of one or more of these critical materials, this in turn could make life every difficult for the car and battery manufacturers in Europe and US (and other parts of the world) who are trying to build their own domestic industries. Chinese restrictions could see prices could shoot up increasing costs for manufacturers, or supplies cut off altogether making manufacturing impossible or uncompetitive.

In fact, China has already started exerting its control of critical materials. In 2023 China cut off the export of the technology that processes rare earth metals. Rare earth metals are needed to build the magnets in EV batteries, and they are used in wind turbines and also jet aircraft. China has cited national security concerns, but many see it as a warning shot.

Graphite

China has also tightened the controls around graphite another material it has a virtual monopoly upon. Graphite is the largest EV battery component by weight, so any market disruption will see higher prices for manufacturers. Beijing’s move was in response to the EU considering tariffs on Chinese built electric vehicles – arguing that they benefit from government subsidies.

China’s move was an explicit warning to the west - challenge us in the electric car market at your peril. In the short term at least there hasn’t been much impact as graphite prices had been falling, and the fear of losing the supply is likely to speed up the search and implementation of new graphite sources. But over the medium and long term as demand for graphite picks up this could change at great cost to manufacturers and to many country’s climate ambitions.

Future Restrictions?

Trivium Group have developed a handy breakdown of which metals and minerals China could target next. Trivium have analysed the situation from Beijing’s viewpoint and have tried to game out which materials are most at risk in a further escalation of the trade war.

For the climate tech industry, the biggest risk appears to be further restrictions on rare earth metals. Widely recognised as a critical material (in reality a wide range of little known, but not actually that rare metals). China controls the 68% of mining and around 85% of the processing of rare earth metals.

Therefore, cutting off rare earth materials would be relatively painless for China which is self-sufficient, but would be extremely painful for the US, Japan and the EU. Currently, the US only has a single facility refining rare earth metals. New mines and processing facilities take many years to become functional.

By imposing restrictions on rare earth metals or other critical materials China can push prices sky high for manufacturers potentially snuffing out competitors’ renewable energy industries. A tempting proposition for a country determined to maintain its dominance in this sector.

Companies and countries keep getting surprised by new restrictions, but they are now an established tool in China’s economic-diplomacy arsenal which will be used again very soon. Identifying and mapping dependency on Chinese trade in supply chains and seeking out alternatives should be a priority for both companies and states.

Limitations on Controls

But supplies chains are hard to control. Western sanctions on Russia were partially effective, but any block on trade creates an opening for middlemen who are eager to fulfil demand. Unless controls can target a single country then they risk alienating friends and allies. But of course unless they are universal applied they will be easily circumnavigated.

Strategic Ambiguity

Perhaps the most powerful weapon in China’s arsenal is using strategic ambiguity around critical materials controls. Maintaining a level of threat and uncertainty around what actions you might take is extremely powerful. It leaves others fearing and trying to guess your next move.

China will continue trying to disrupt the critical mineral market by making further export controls. The hope is that it will scare the EU, US and others into avoiding or reversing any anti-Chinese economic measures such as tariffs or investment restrictions.

Ultimately Beijing will avoid creating excessive disruption in the critical mineral market because it does not want to force other countries outside of its supply chains completely, and does not want to use it all its cards except perhaps in the event of major conflict in East Asia. Much better to utilise strategic ambiguity and keep competitors guessing.